LoanBaazar is excel in offering Home Loan, Mortgage Loan, Business Loan, Personal Loan, Education Loan, Credit Cards, SME Working Capital Loan and Equipment Finance at the most competitive rates from all leading Banks and NBFCs.

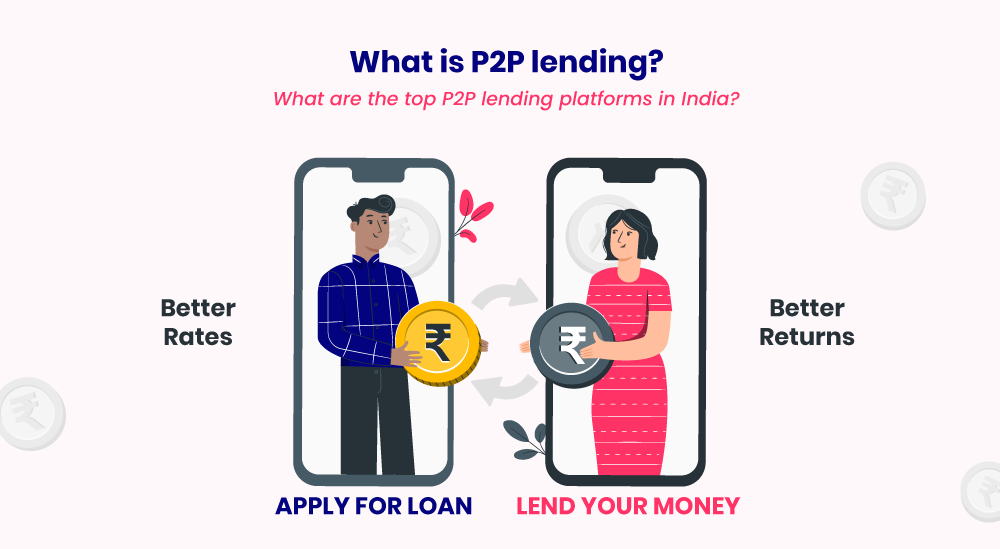

Peer-to-Peer (P2P) lending platforms, operating as Non-Banking Financial Companies (NBFCs), have gained popularity in India as an alternative source of borrowing. These platforms connect borrowers directly with lenders, offering a streamlined process and competitive interest rates. However, like any financial transaction, there are risks involved. This article aims to provide an in-depth analysis of borrowing from P2P lending NBFCs in India, examining the risks associated with this form of borrowing, as well as the advantages it offers to borrowers. By understanding both sides of the equation, borrowers can make informed decisions and mitigate potential risks.

I. Understanding P2P Lending NBFCs in India

A. P2P Lending NBFCs Explained: P2P lending NBFCs are financial institutions registered with the Reserve Bank of India (RBI) that operate as intermediaries between borrowers and lenders on P2P lending platforms. These platforms facilitate loan transactions, connecting individuals seeking loans with lenders looking to invest their funds. P2P lending NBFCs provide the necessary infrastructure, credit assessment, and loan servicing.

B. Regulatory Framework: The RBI introduced guidelines in 2017 to regulate P2P lending platforms operating as NBFCs. These guidelines focus on ensuring transparency, fair practices, and risk mitigation. P2P lending NBFCs must comply with operational, prudential, and customer protection norms set by the RBI.

II. Advantages of Borrowing from P2P Lending NBFCs in India:

A. Access to Credit: P2P lending NBFCs offer a viable alternative for borrowers who may have difficulty accessing credit through traditional financial institutions. These platforms cater to individuals with limited credit history, self-employed individuals, or those who may not meet the stringent criteria set by banks. Borrowers can explore loan options tailored to their specific needs.

B. Competitive Interest Rates: P2P lending NBFCs introduce competition into the lending market, potentially leading to more competitive interest rates compared to traditional lenders. Borrowers have the opportunity to secure loans at lower rates, reducing their overall cost of borrowing.

C. Quick and Convenient Process: P2P lending NBFCs leverage technology to streamline the borrowing process, offering quick and convenient loan approvals. Borrowers can complete the application process online, eliminating the need for lengthy paperwork and physical visits to financial institutions. The digital platform enables borrowers to connect directly with potential lenders, expediting the loan disbursal process.

D. Diverse Loan Options: P2P lending NBFCs provide borrowers with a range of loan options to suit their requirements. Whether it’s personal loans, business loans, education loans, or other specific purposes, borrowers can find lenders willing to fund their loan requests. The platform allows borrowers to access loans with flexible terms and repayment options.

III. Risks Associated with Borrowing from P2P Lending NBFCs:

A. Credit Risk: One of the primary risks in P2P lending is the potential for default by borrowers. P2P lending NBFCs assess the creditworthiness of borrowers; however, there is no guarantee that all borrowers will repay their loans. Borrowers should carefully consider their ability to repay and choose loan amounts that align with their financial capacity.

B. Limited Regulatory Protection: While P2P lending NBFCs in India operate under the regulatory framework set by the RBI, it’s important to note that the level of regulatory protection may not be as comprehensive as that provided by traditional financial institutions. Borrowers should understand the terms and conditions of the loan agreement and the platform’s dispute resolution process.

C. Platform Reliability and Fraud Risk: Borrowers should exercise caution while selecting P2P lending NBFCs and verify the credibility and reliability of the platforms. There is a risk of fraudulent platforms operating in the market. It is advisable to choose platforms that have established a strong track record, maintain transparent operations, and have robust security measures in place.

D. Lack of Secondary Market Regulation: The secondary market for P2P loans, where borrowers may wish to exit their loans early, is relatively unregulated in India. Borrowers should be aware that liquidity may be limited and there could be challenges in finding buyers for their loan parts.

E. Interest Rates and Fees: While P2P lending NBFCs can offer competitive interest rates, borrowers should carefully review the terms and conditions of the loan. Some platforms may charge processing fees, origination fees, or other charges that borrowers should factor into their overall cost of borrowing.

IV. Mitigating Risks and Best Practices:

A. Conduct Due Diligence: Before borrowing from a P2P lending NBFC, borrowers should conduct thorough due diligence on the platform. Research the platform’s reputation, track record, and customer reviews. Look for platforms that have transparent processes, comprehensive risk assessment mechanisms, and robust customer support.

B. Understand the Loan Agreement: Carefully read and understand the loan agreement, including interest rates, repayment terms, fees, and any potential penalties for late payments or defaults. Seek clarification on any aspects that are not clear before proceeding with the loan.

C. Assess Repayment Capacity: Borrowers should assess their repayment capacity realistically. Consider factors such as income stability, existing financial obligations, and potential changes in circumstances. Borrow within your means to ensure timely repayments and avoid default.

D. Diversify Loan Requests: To mitigate the risk of default, consider diversifying loan requests across multiple lenders. This strategy reduces the impact of a single borrower defaulting and helps spread the risk.

E. Maintain Communication: Maintain open communication with the platform and lenders throughout the loan tenure. Inform them promptly about any changes in financial circumstances or difficulties in repaying the loan. Timely communication can help explore potential solutions and prevent adverse consequences.

Conclusion:

Borrowing from P2P lending NBFCs in India offers advantages such as access to credit, competitive interest rates, convenience, and diverse loan options. However, borrowers should be aware of the risks associated with this form of borrowing, including credit risk, limited regulatory protection, platform reliability, lack of secondary market regulation, and interest rates and fees. By adopting best practices, conducting due diligence, understanding loan agreements, assessing repayment capacity, and maintaining communication, borrowers can mitigate potential risks. P2P lending NBFCs have the potential to provide a valuable borrowing option for individuals who may face challenges with traditional lenders. It is crucial for borrowers to exercise caution, make informed decisions, and choose reputable platforms that prioritize transparency and customer protection.

Disclaimer: LoanBazaar or any of its associates will never request any payment to process or approve a loan. If any individual or organization demands such payment, they are doing so at their own risk, and LoanBazaar will not be held responsible for their actions. We advise our customers to be cautious and to report any such demands to us immediately. Loan approval is subject to meeting the eligibility criteria and following the application process, which may include the submission of required documents. LoanBazaar reserves the right to reject any loan application that does not meet our internal policies and procedures. The information provided on LoanBazaar's platform is for informational purposes only and should not be considered as financial or legal advice. The borrower is responsible for reviewing and understanding the terms and conditions of any loan agreement before accepting it. LoanBazaar will not be liable for any financial loss or legal issues that may arise from the borrower's use of any loan product or lender found through our platform.